Autocorrelation

The purpose of this section is to show that OLS is not an efficient estimator when there is autocorrelation in the error term; instead, the GLS is better.

Assuming \(y_t\) can be written as a linear function of \(x\) and the error term \(\epsilon\) has autocorrelation \[y_t = 1.2 + 2.2 x_{1,t} + 2.3 x_{2,t} + \epsilon_t \] \[ \epsilon_t = \rho \epsilon_{t-1} + w_t ,\, where\, w \sim N(0,\sigma^2)\] To simulate \(y\) we do:

#install.packages("matrixStats")

library(MASS)

library(matrixStats)

m=50

x <- mvrnorm(n=m,mu=c(0.05,0.08),

Sigma=matrix(c(0.0004,0.00023,0.00023,0.0006),

nrow=2,ncol=2,byrow=TRUE))

## assuming correlation in x

et <- arima.sim(list(order = c(1,0,0),ar=0.8),n=m,rand.gen=rnorm,sd=0.1)

yt <- 1.2 + x %*% c(2.2,2.3)+et1. OLS

Then we do regress \(y\) on \(x\) using OLS:

regressY <- lm(yt~x)

summary(regressY)##

## Call:

## lm(formula = yt ~ x)

##

## Residuals:

## Min 1Q Median 3Q Max

## -0.210733 -0.075193 -0.002246 0.082349 0.152111

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 1.29574 0.05106 25.376 < 2e-16 ***

## x1 2.76363 0.66160 4.177 0.000127 ***

## x2 1.52826 0.59561 2.566 0.013541 *

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 0.09152 on 47 degrees of freedom

## Multiple R-squared: 0.4218, Adjusted R-squared: 0.3972

## F-statistic: 17.14 on 2 and 47 DF, p-value: 2.565e-06regressY$coefficients## (Intercept) x1 x2

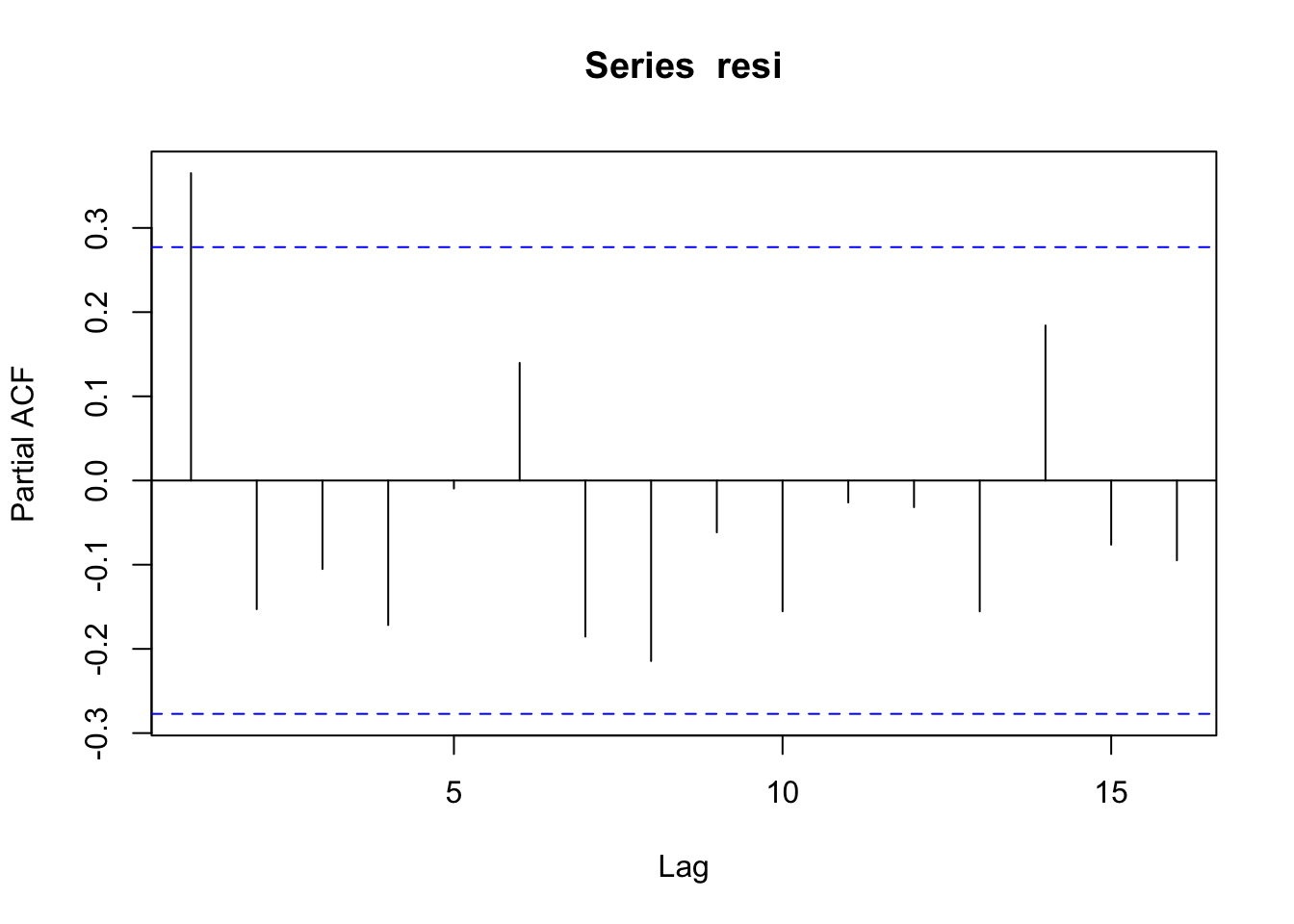

## 1.295744 2.763632 1.528259Test the autocorrelation of residuals

resi <- regressY$residuals

pacf(resi)

ar.ols(resi)##

## Call:

## ar.ols(x = resi)

##

## Coefficients:

## 1 2 3 4 5 6 7 8

## 0.2506 -0.2385 -0.0872 -0.2247 -0.1210 0.1331 -0.0703 -0.1665

## 9 10

## -0.0445 -0.2467

##

## Intercept: 0.007674 (0.0114)

##

## Order selected 10 sigma^2 estimated as 0.004622. GLS

GLS with AR(1) residuals is actually OLS on the below equation:

\[y_t - \rho y_{t-1} = \alpha (1-\rho) + \beta_1(x_{1,t} - \rho x_{1,t-1}) + \beta_2 (x_{2,t} - \rho x_{2,t-1}) + w\]

## regress on resi hat

regressE <- lm(resi[2:length(resi)]~resi[1:(length(resi)-1)]-1)

rho <- regressE$coefficients[1]

## GLS

## yt - rho * yt_1 = alpha * (1-rho) + beta1*(x1_t - rho * x1_t-1) + beta *

## (x2_t - rho * x2_t-1)

yt2 <- yt[2:length(yt)]

xt2 <- x[2:nrow(x),]

xprime <- (xt2- c(rho,rho) * x[1:(nrow(x)-1),])

regressY_GLS <- lm( (yt2-rho*yt[1:(length(yt)-1)]) ~ xprime)

summary(regressY_GLS)##

## Call:

## lm(formula = (yt2 - rho * yt[1:(length(yt) - 1)]) ~ xprime)

##

## Residuals:

## Min 1Q Median 3Q Max

## -0.177314 -0.071225 -0.003311 0.061894 0.159587

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 0.81056 0.03086 26.263 < 2e-16 ***

## xprime1 2.75543 0.57350 4.805 1.69e-05 ***

## xprime2 1.80830 0.56190 3.218 0.00237 **

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 0.08437 on 46 degrees of freedom

## Multiple R-squared: 0.5235, Adjusted R-squared: 0.5027

## F-statistic: 25.26 on 2 and 46 DF, p-value: 3.947e-08alpha <- regressY_GLS$coefficients[1]/(1-rho)

alpha## (Intercept)

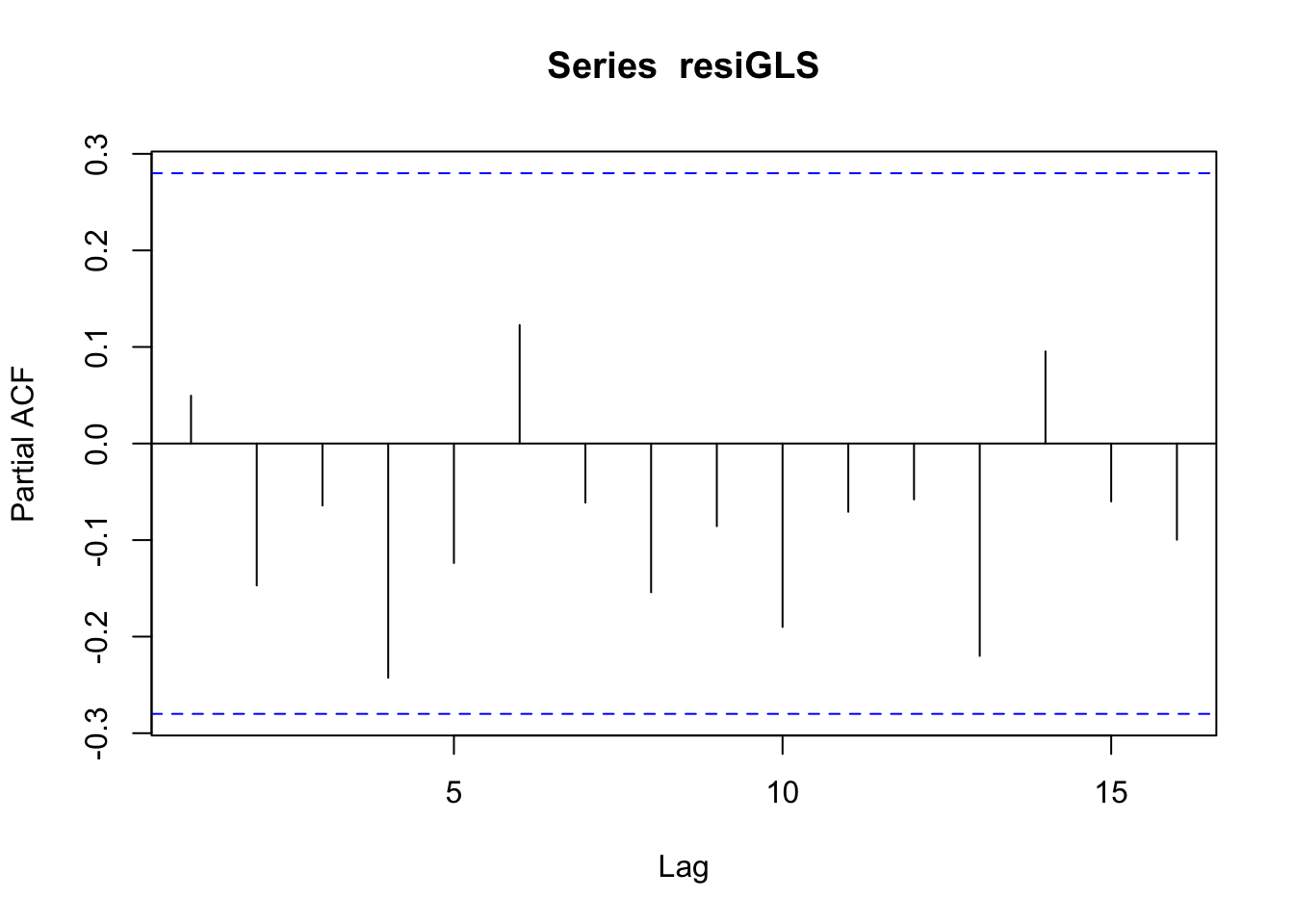

## 1.276583See if the residuals of GLS has autocorrelation:

resiGLS <- regressY_GLS$residuals

pacf(resiGLS)

3. Run n times

We redo the above steps for n times to observe the sampling distribution of OLS and GLS estimators:

n=2000

OLS_coefs <- matrix(nrow=n,ncol=3)

GLS_coefs <- matrix(nrow=n,ncol=3)

for(i in 1:n) {

x <- mvrnorm(n=m,mu=c(0.05,0.08),

Sigma=matrix(c(0.0004,0.00023,0.00023,0.0006),

nrow=2,ncol=2,byrow=TRUE))

## assuming autocorrelation in x

et <- arima.sim(list(order = c(1,0,0),ar=0.8),n=m,rand.gen=rnorm,sd=0.1)

yt <- 1.2 + x %*% c(2.2,2.3)+et

regressY <- lm(yt~x)

#summary(regressY)

OLS_coefs[i,] <- regressY$coefficients

## GLS

resi <- regressY$residuals

regressE <- lm(resi[2:length(resi)]~resi[1:(length(resi)-1)])

rho <- regressE$coefficients[2]

## GLS

## yt - rho * yt_1 = alpha * (1-rho) + beta1*(x1_t - rho * x1_t-1) + beta *

## (x2_t - rho * x2_t-1)

# yt2 <- yt[2:length(yt)]

# xt2 <- x[2:nrow(x),]

# xprime <- (xt2- c(rho,rho) * x[1:(nrow(x)-1),])

# regressY_GLS <- lm( (yt2-rho*yt[1:(length(yt)-1)]) ~ xprime)

# alpha <- regressY_GLS$coefficients[1]/(1-rho)

# GLS_coefs[i,1] <- alpha

# GLS_coefs[i,2:3] <- regressY_GLS$coefficients[2:3]

GLS_coefs[i,] <- CochraneOrcuttIteration(yt,x,0.001)

}

colMeans(OLS_coefs)## [1] 1.199079 2.213421 2.291709colMeans(GLS_coefs)## [1] 1.199158 2.212982 2.289499The variance of the sampling distribution of GLS is much smaller than that of the OLS, and is therefore more effieicnt.

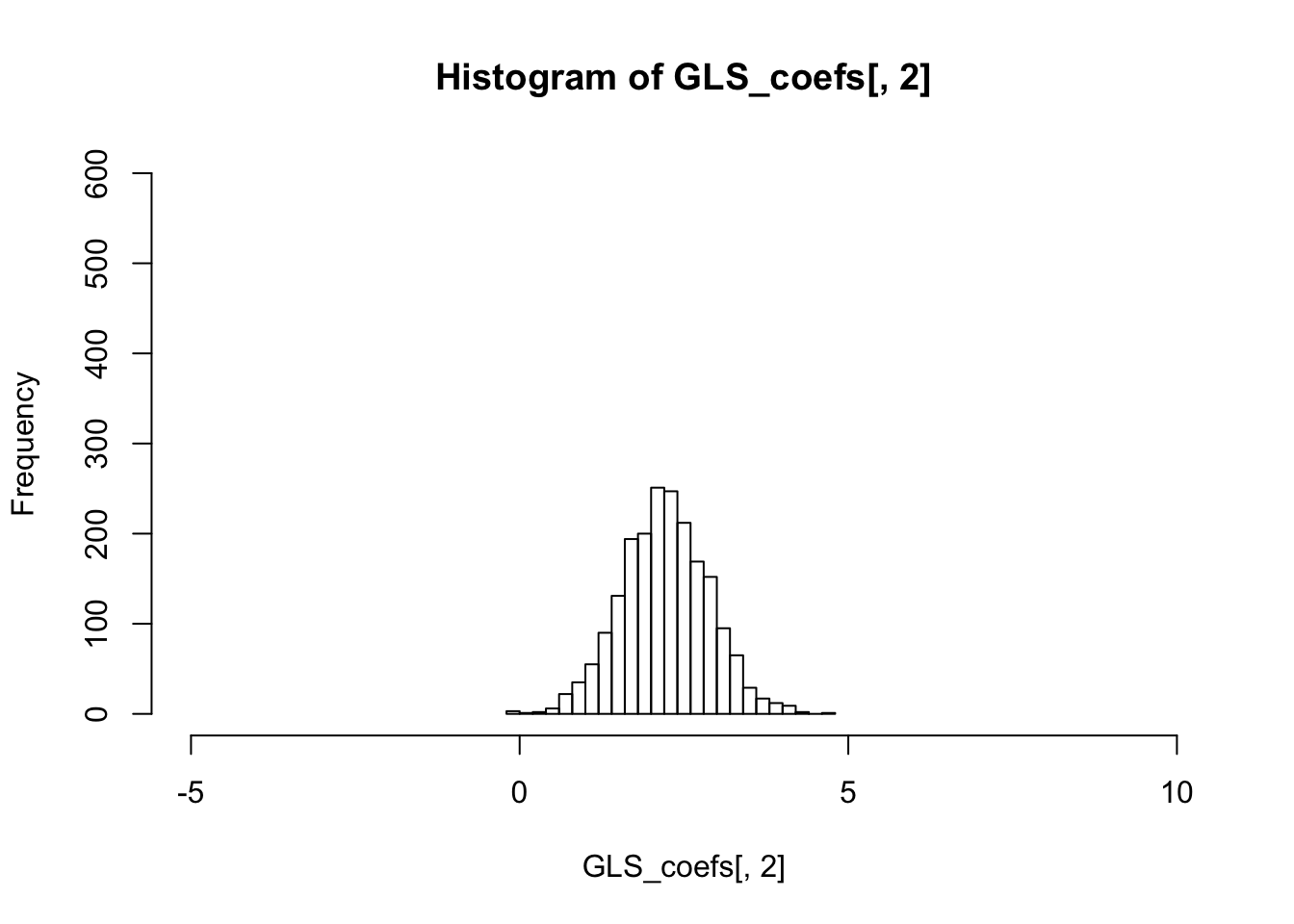

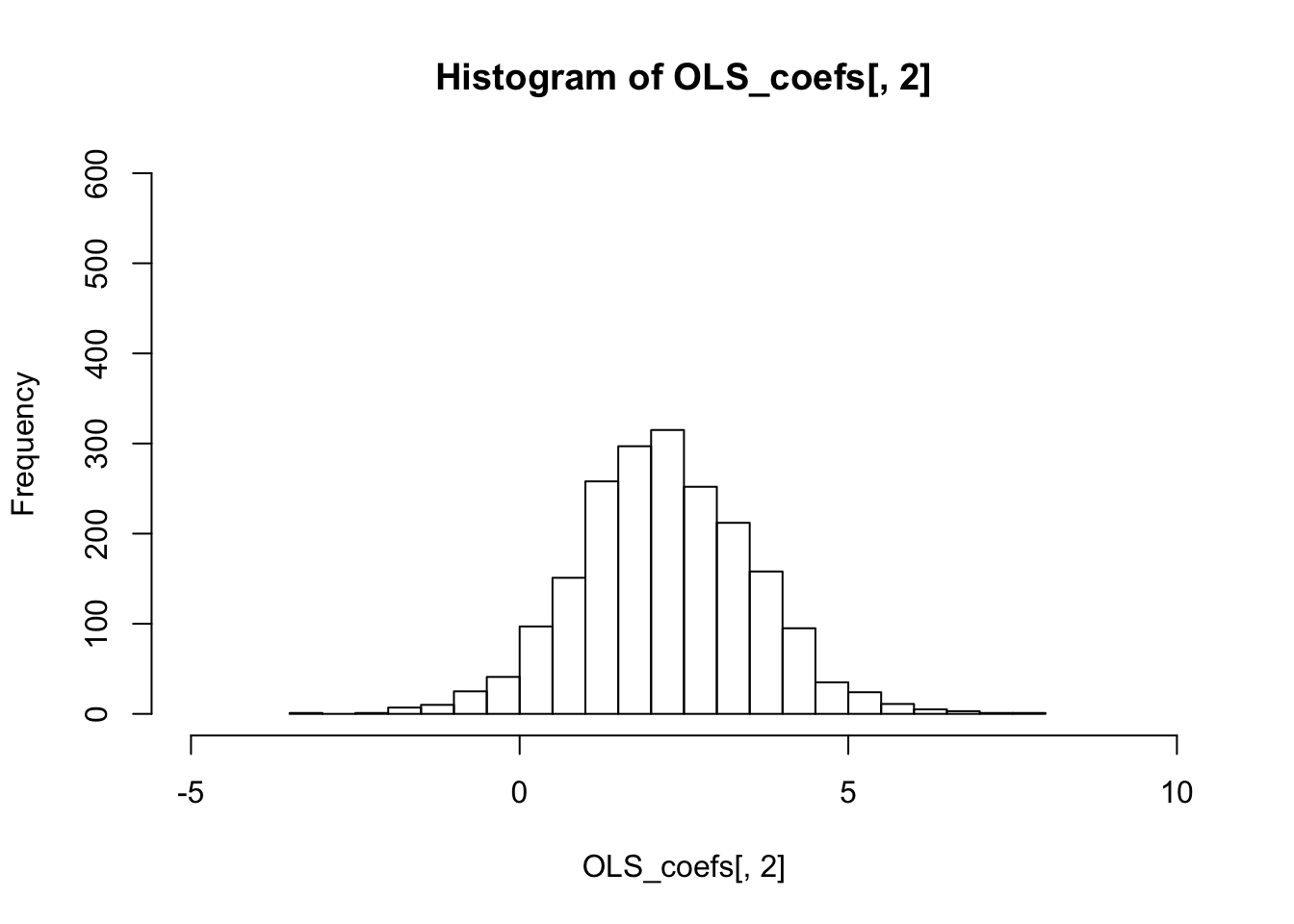

colVars(OLS_coefs)## [1] 0.01033834 1.78235434 1.08553247colVars(GLS_coefs)## [1] 0.007005371 0.441118007 0.276296824hist(OLS_coefs[,2],breaks=20,xlim=c(-5,10),ylim=c(0,600))

hist(GLS_coefs[,2],breaks=20,xlim=c(-5,10),ylim=c(0,600))